Tom King, 63, was the only member of the Silicon Valley Bank board who had experience in investment banking. The others were major Obama and Clinton mega-donors, including one who cried when Trump won in 2016. The board is now being investigated for its failure to act ahead of the bank’s collapse, as some argue it was too focused on being woke.

Just one member of Silicon Valley Bank’s board of directors had a career in investment banking, while the others were major Democratic donors, it has been revealed.

Tom King, 63, was appointed to the board in September after previously serving as the CEO of investment banking at Barclay’s. He has had 35 years of experience in investment banking.

But he is the only one on the board with a career in the financial industry, while others are a former Obama administration employee, a prolific contributor to former House Speaker Nancy Pelosi and even a Hillary Clinton mega-donor who prayed at a Shinto shrine when Donald Trump won the 2016 presidential election.

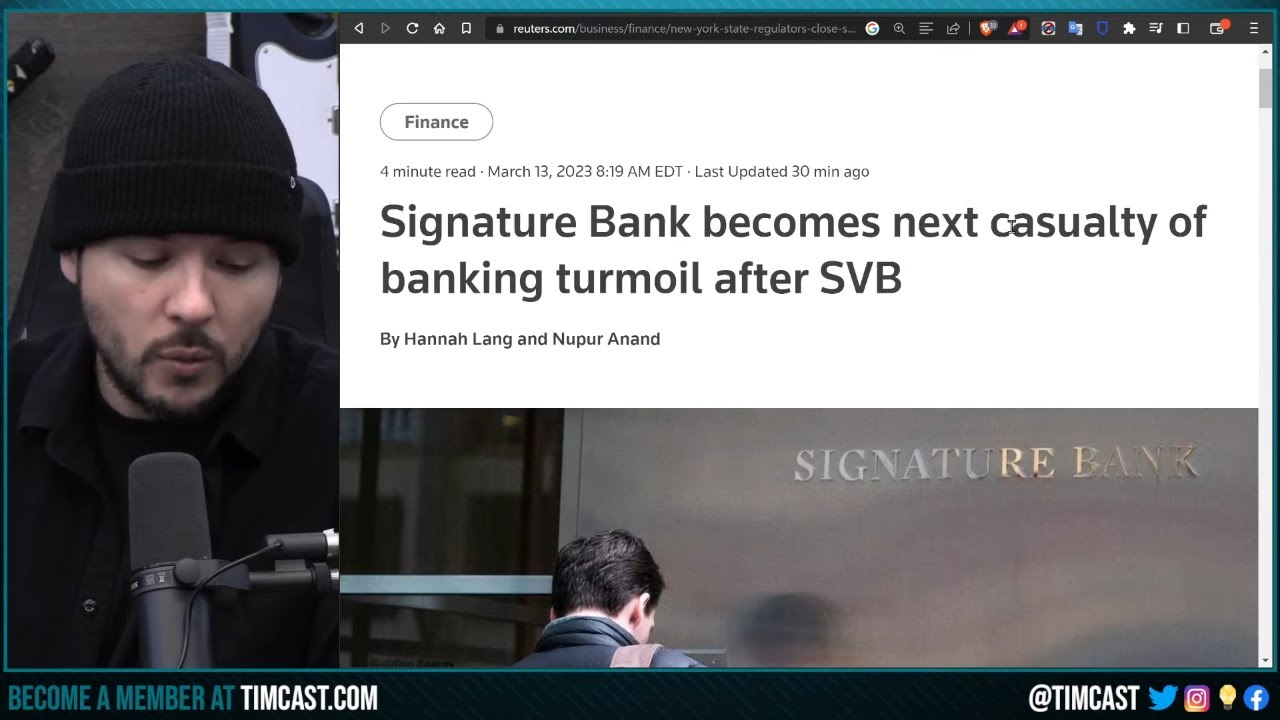

The board is now being investigated by federal authorities after it failed to prevent the bank from going under while it was investing clients’ money in risky low-interest government bonds and securities.

[…]